Words by Gabriel Zanko, Tech Advisor, CEO of MobileyourLife ( Investment Banking for Deep Technology and Renewable Energy), CEO of Urano Capital( the future Seed Fund for Deep Technology), researcher and speaker

Daniel Ramos, Gabriel Zanko, Mobileyourlife – Bogotá, D.C., Colombia

Abstract

In one of our previous releases, we covered certain events that were considered possible catalyzers of a rise in the popularity and relevance of the Decentralized Finance (DeFi) sector within the market of cryptocurrency and digital assets. Since then, multiple events have fortified the positive sentiment towards relevant platforms and some of these offer new services to fulfill the needs of current and new users.

INTRODUCTION

Nearly three months ago we released our first research document summarizing the state of DeFi at the time1, in which we focused on giving an introduction to this booming sector of the cryptocurrency market, along with certain events that appeared to be trend-setting for the upcoming months, along with important concepts required to understand most analyses on this market.

The most important concept to refresh is the Total Value Locked, a metric used to quantify the relevancy of the market as a whole and of individual platforms, regardless of the type of service they provide. The TVL is calculated by the total amount of tokens stored in the contracts of a platform, multiplied by the value of each token in a currency (which is usually USD or ETH).

The use of this metric is especially useful for DeFi since just looking at the value, market capitalization or trading volumes of their tokens does not include the amounts agreed to be transacted in smart contracts. Given that the popularity of a platform can be equated to the number of current contracts in it, using TVL to compare the performance of a platform gives a more accurate insight on its current situation.

Another aspect we covered in our previous release is the variety of different services to which users have access in DeFi. Since most of the platforms are built on the Ethereum network, they can take full advantage of the smart contracts functionalities to offer services that imitate or even surpass those offered by regular banking institutions. From Compound’s pool-based lending service to creating digital assets tethered to the value of real ones, the world of DeFi appears to have a nearly limitless potential for growth, and in this document, we will review how much of this potential managed to be materialized in the last two months, along with relevant releases and covering the platforms that appear to dictate the sentiment of the public and, consequently, the state of the market.

OVERALL STATE

Compared to what we reported a couple of months ago, DeFi has grown at an incredibly healthy rate, supported by an increase in the number of open contracts – which can translate into an increase in either the number of users or the activity of the already existing users – and a steady climb in the overall TVL of the market.

Despite the fact that the accepted catalyzer of this strong positive trend is Compound’s release of their platform to an entirely decentralized governance system through their COMP token, the relevance of the platform has decreased gradually and the growth of the market has been driven by important launches andreleases in other competitive platforms, along with a new trend of “yield farming”.

Despite the fact that the accepted catalyzer of this strong positive trend is Compound’s release of their platform to an entirely decentralized governance system through their COMP token, the relevance of the platform has decreased gradually and the growth of the market has been driven by important launches andreleases in other competitive platforms, along with a new trend of “yield farming”.

Among the most relevant releases in these months, the launch of AAVE v2, the second version of the platform that allows their users to create digital assets and tether their value to real life assets. On top of the basic functionalities of the original version, what boosted their popularity is the option to swap collateral and debt between tokens, which they consider as the first step towards replicating complex lending mechanisms such as mortgages.

Another important aspect to consider is how reliable these tendencies can be in the mid- to long-term, which is considerably harder considering how volatile the cryptocurrency market can be. However, there are indicators that can be used to paint a picture, which include daily trading volumes and open interests, two metrics that have been associated with trend strength for around two decades, especially when studying the futures market.

Studies on the effects of events2,3 like acquisitions and earnings announcements on trading volumes, defined as the total amount of value that is moved in transactions, indicate that they tend to increase as rumors of these “positive” events become widespread, and decrease after the event occurs or, in case of rumors, is denied. However, open interests (the total amount of outstanding contracts at any given time) work as an indicator of trend strength4 since an increase in this metric indicates more activity from existing users or an influx of new traders.

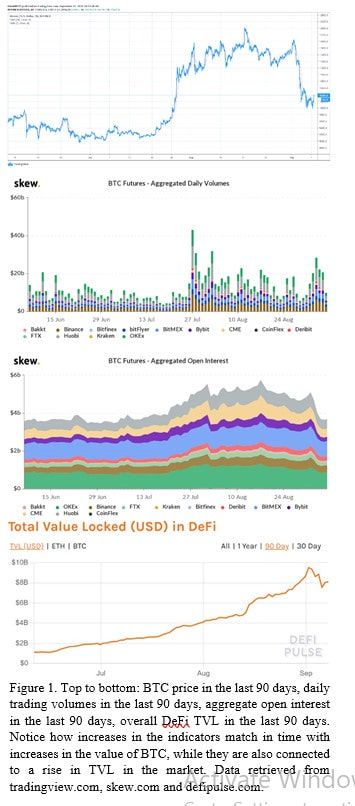

When translated to the cryptocurrency derivatives market, the second largest fraction of DeFi and one that offers important information about the state of the overall sector, these indicators take additional meaning. For example: looking at the trading volumes and open interests in the last 3 months, we can see a noticeable spike in the days surrounding July 27th. When compared to the price of BTC, the most dominant cryptocurrency in the market by a long margin, we can also see an increase. There is a clear correlation between the behavior of the token and the movements of the indicators, but a sense of causality is more difficult to ascertain, since there are many other factors that may influence the price of Bitcoin and, by extension, the overall value of the cryptocurrency market.

When applying these criteria to the current state of DeFi compared to our previous release, we can see an overall increase in the average trading volumes and open interests compared to the state at that moment, which translates into a surge in activity, possibly triggered by the success of launches and announcements of many important platforms in the market. Looking at the TVL for the last 3 months, we can see a change in the rate of growth since the last days of July, which matches the increases in trading volume and open interests, strengthening the theory that an increase in these indicators is often accompanied by a rise in TVL and vice versa, as seen in the last couple of days.

However, since DeFi is a market that is mostly defined by the services offered to the users by the different platforms, it is also important to look at the state of the individual platforms when trying to define the current state of the market as certain announcements or rumors have had significant effects on it.

IMPORTANT PLATFORMS

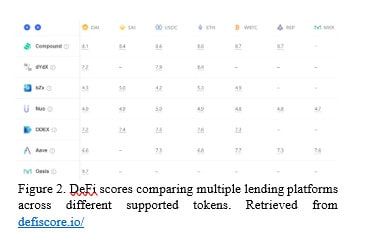

When defining a platform as “important” within the DeFi market, there are different approaches: ranking them by TVL or daily trading volume can give us a picture of how relevant the platform currently is, but other factors may give away additional information depending on the type of the platform, like how “DeFi score” can quantify the associated risks in lending protocols so they can be compared5. Based on a combination of these factors, the platforms considered to be the most relevant at the time are the following:

Compound

Launched in 2017, Compound has always been regarded as a relevant DeFi platform thanks to their innovative pool-based lending system, where users that deposit an amount in any of the supported cryptocurrencies are given a number of cTokens on top of which they can accumulate interest. These cTokens also work as a collateral to determine the maximum amount a user can borrow at a certain moment.

With the release of their COMP token in late June6, and so turning their platform into an entirely decentralized one where COMP holders have a vote into the important decisions of the platform, Compound brought the attention of the cryptocurrency world to DeFi as a sector with incredible potential for growth and self-governance. This launch is said to be the vent that broke the $1 billion resistance level of the overall TVL, and DeFi has only kept growing ever since.

With the release of their COMP token in late June6, and so turning their platform into an entirely decentralized one where COMP holders have a vote into the important decisions of the platform, Compound brought the attention of the cryptocurrency world to DeFi as a sector with incredible potential for growth and self-governance. This launch is said to be the vent that broke the $1 billion resistance level of the overall TVL, and DeFi has only kept growing ever since.

As expected, the hype behind this launch fell under control after a couple of weeks, and Compound’s TVL is currently around $470 million, as users took advantage of their model to generate passive income but traded more actively in other platforms. However, it still holds the highest score among lending platforms due to the low risk associated to their model and the wide variety of supported tokens.

Maker

Regarded as the first important DeFi platform, Maker offers a simpler lending model compared to Compound, where the supported DAI token, a stablecoin with a unique approach as it is a truly decentralized stablecoin. It is not backed nor pegged to the U.S. dollar nor any central authority like USDT and truly lives on the blockchain, backed by ETH, another decentralized cryptocurrency. Users can use the platform to create a Vault, lock collateral in other supported tokens and generate DAI in interests against the collateral.

Since their launch in late 2017, and being worked on for nearly 3 years before its launch according to their team7, it has been a staple in the DeFi market in terms of users and TVL, holding over 40% dominance for most of its existence. This large number of users is what helped the platform to recover after Compound’s overtake, and it now holds the second highest TVL of around $1 billion, but its score as a lending platform is lower compared to Compound.

The most relevant feature of Maker is how their second native token, MKR, has multiple purposes, basically working as the pillar on top of which the platform works. It not only serves the function of a governance token, but it is also how DAI is kept from fluctuating too far from its intended value. Given that, in case of an automatic liquidation, the provided collateral might drop value and leave an unpaid amount, the system is programmed to mint and sell new MKR (within the established maximum amount of 1,000,000), in order to cover the potential loses that may cause DAI to fluctuate.

The most relevant feature of Maker is how their second native token, MKR, has multiple purposes, basically working as the pillar on top of which the platform works. It not only serves the function of a governance token, but it is also how DAI is kept from fluctuating too far from its intended value. Given that, in case of an automatic liquidation, the provided collateral might drop value and leave an unpaid amount, the system is programmed to mint and sell new MKR (within the established maximum amount of 1,000,000), in order to cover the potential loses that may cause DAI to fluctuate.

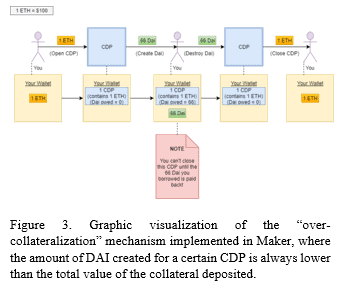

On top of that, all the minted DAI coins are over- collateralized, meaning that there is a collateralization ratio greater than 1:1 which prevents situations of unpayable debt due to a devaluation of the underlying asset. An example of this system is shown in Figure 3, showing how a CDP of 1 ETH could be created and, if ETH is worth $100 and the collateralization ratio is at 1.5:1, only 66 DAI can be created.

These mechanisms were created in hopes of overcoming the volatility of cryptocurrency, as the team has analyzed real scenarios of extreme fluctuation in their whitepaper8. With a system that has proven the attractiveness of a truly decentralized and stable token and its importance as the cornerstone of a solid and efficient lending system.

AAVE

The current top protocol in DeFi, AAVE is a Finnish platform that started as a P2P lending project in 2017 (ETHLend), rebranded in 2018 and launched their Ethereum-based lending system in January 2020. Their platform allows users to mint aTokens at a 1:1 ratio to the supplied assets, which generate new aTokens as compound interests constantly since their creation.

They also offer several attractive lending systems, like their “flash loans” where the borrowing and repayment must occur on the same transaction but can be requested in an uncollateralized way. However, what made them claim the first spot in TVL was the launch of the second version of their platform (v2), which introduced a variety of quality-of-life improvements to their users, including the ability to repay loans with collateral, debt tokenization and swap, fixed rate deposits and the permission to create private markets within the protocol, along with improvements in transactions fees and security.

Synthetix

Being the only non-lending platform on the high spots in the market, Synthetix holds special importance in upholding the variety of DeFi. This decentralized exchange’s main offer is the creation of Synths, digital tokens that track the value of a real-world asset. This brings the benefits of DeFi to the management of traditional assets, which is an important step towards true decentralized digitization of these assets.

The constant growth in the list of supported assets is key in keeping Synthetix relevant, with an already strong catalog that supports Synths tethered to fiat currencies, commodities (e.g. gold) and other cryptocurrencies, with the unique distinction of supporting tokens that track values inversely (e.g. iUSD, iEUR).

FORESEEABLE FUTURE

With the rise in value of DeFi, an improvement in the public’s opinion towards the market was expected, but an increase of nearly ten times in the span of a few months was certainly more than what was envisioned, and could also be considered a red flag.

The volatility in trading volumes and open interests paints a picture of mostly short-term contracts or contracts established with very sensible exit conditions being created. This, combined with the widespread of a practice known as “yield farming” (the act of performing multiple fast transactions across platforms to generate income on each trade), indicates that the current environment is mostly populated by uncommitted users who are probably profiting off of the increased hype around DeFi, but the long-term effects of these practice could ultimately become beneficial for the market.

On the other hand, DeFi is still closely related to cryptocurrencies, and such a volatile environment can generate incredibly high spikes or sudden drops, even though smart contracts and derivates are usually less time-sensitive than pure cryptocurrency trading. One should never think of DeFi as a completely isolated market, much like crypto is not entirely protected against events that affect the traditional economic systems, but there are clear advantages associated to the services offered by DeFi platforms when compared to regular trading.

REFERENCES

Ramos, D., Zanko, G. (2020) “A Review of Decentralized Finance as an Application of Increasing Importance of Blockchain Technology”. MobileyourLife.

Jayaraman, N., Frye, M.B. and Sabherwal, S. (2001), “Informed Trading around Merger Announcements: An Empirical Test Using Transaction Volume and Open Interest in Options Market.” Financial Review, 36: 45-74.

Donders, M.W., Kouwenberg, R. and Vorst, T.C.F. (2000), “Options and earnings announcements: an empirical study of volatility, trading volume, open interest and liquidity.” European Financial Management, 6: 149-171.

Bhuyan, R., Chaudhury, M. (2005), “Trading on the information content of open interest: Evidence from the US equity options market.” J Deriv Hedge Funds 11, 16–36.MakerDAO (2017), “The Maker Protocol: MakerDAO’s Multi-Collateral Dai (MCD) System”. Retrieved from https://makerdao.com/en/whitepaper/

About Affiliate Grand Slam:

Affiliates are gold in the iGaming industry and the SiGMA Affiliate Grand Slam is our own bespoke Affiliate Club that gathers all major, upcoming and affiliate startups within the industry. Being part of the SiGMA Affiliate Grand Slam will ensure that as an affiliate you will automatically qualify and benefit from what we at SiGMA, being the world’s largest iGaming festival, can provide you with. It’s free to join the SiGMA Affiliate GrandSlam. Affiliates requesting to join will be vetted through a membership application process upon submitting a request to JOIN.