What you need to know about Flutter’s takeover of Snaitech

In a deal that promises to reshape Italy’s gambling landscape, Flutter Entertainment has announced its acquisition of Snaitech (Snai), an Italian omni-channel operator, for €2.3 billion. This strategic acquisition will expand Flutter’s already significant footprint in Europe’s largest gambling market. With Italy’s gross gaming revenue (GGR) forecasted to hit €21 billion in 2023, the stakes are high. Here’s a detailed look at the implications of this acquisition and why it’s set to enhance Flutter’s competitive position in Italy.

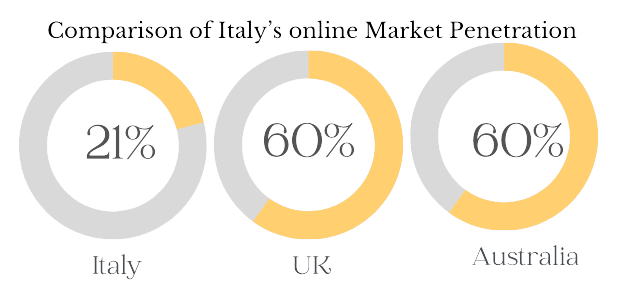

Italy has been an attractive target for many global gaming companies, and for good reason. It is the largest regulated gambling market in Europe, with an enormous potential for digital growth. As of 2023, only 21 percent of Italy’s market GGR came from online channels, a huge contrast to mature markets like the UK and Australia, where online penetration exceeds 60 percent. This underlines a critical opportunity for growth, as the Italian market is expected to see a compound annual growth rate (CAGR) of approximately 10 percent in online gaming over the next three years. Flutter’s strategic entry into this relatively underdeveloped online market through Snai is not just timely, but also potentially transformative.

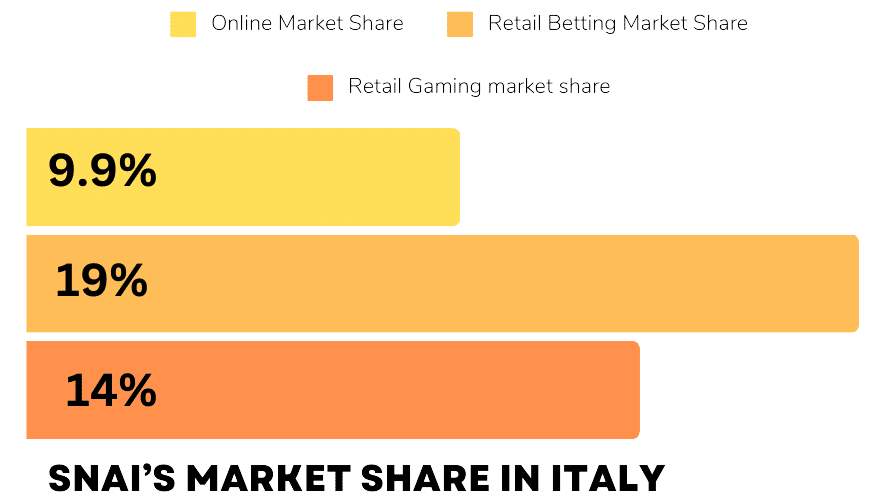

Snai, with a 9.9 percent online market share and 291,000 average monthly players, ranks as the third-largest online operator in Italy. But it’s not just about digital presence. Snai’s vast retail network, comprising over 2,000 sites, has helped it secure a 19 percent market share in retail betting and a 14 percent share in retail gaming. This omni-channel capability gives Flutter a significant edge, allowing it to leverage both online and offline assets in a market where consumers still gravitate toward physical outlets for deposits and withdrawals.

One of the key elements driving this acquisition is the synergy potential. Flutter expects to realise operating cost synergies of at least €70 million through the integration of technology, procurement, and content between Snai and the Flutter Group. These synergies are expected to be achieved within three years post-completion, with 10 percent of the benefits realised in the first year and 50 percent in the second year. On the revenue side, Flutter is aiming for even more impressive results by leveraging its proprietary technology platform—known as the “Flutter Edge”—to boost pricing, risk management, and in-house casino content, further enhancing the customer experience.

Flutter has an enviable track record of extracting value from acquisitions. The Sisal acquisition serves as a prime example, where the company achieved revenue synergies of 17 percent between Q2 2022 and Q2 2024. With Snai, Flutter expects similar results. The company’s proprietary platform not only provides technological advantages, but it also unlocks economies of scale and delivers improved user experiences, which are critical to driving customer loyalty and growth. This is essential in Italy, where Snai already enjoys a high brand recognition of 74 percent, the third most recognised brand in a heavily regulated market with stringent advertising restrictions.

Financial impact and shareholder value

The acquisition is expected to be immediately accretive to Flutter’s earnings per share, signalling its near-term profitability. With Snai generating €947 million in regulated revenue and €256 million in adjusted EBITDA in 2023, of which 50 percent was generated online, the acquisition significantly boosts Flutter’s top line. This move strengthens Flutter’s balance sheet and supports its broader strategy of pursuing acquisitions that create long-term shareholder value.

On a post-synergy basis, the deal presents an attractive multiple, similar to Flutter’s prior acquisition of Sisal. Moreover, the cost to achieve the projected synergies is expected to be relatively modest at 1.25x, which further underlines the financial prudence of this transaction. With a leverage ratio of 2.6x as of 30 June, 2024, and $5.5 billion of net debt, Flutter is well positioned to manage this acquisition. Although the company’s leverage will increase in the short term, its management expects it to decrease rapidly given the strong profit potential from both organic and acquired growth opportunities.

Positioning for long-term growth

One of the most compelling aspects of this acquisition is how it positions Flutter for long-term growth in Italy and beyond. Italy remains a growth frontier for digital gaming, and Snai’s extensive retail network gives Flutter a unique advantage in combining online and offline channels. The company will capitalise on Snai’s existing infrastructure to drive online penetration, a key growth lever in a market where digital gaming is still in its nascent stages.

Furthermore, Flutter’s multi-brand strategy—already successful in the UK and Australia—will play a vital role in Italy. Snai’s retail dominance, combined with Sisal’s leadership as the most recognised brand in Italy, provides a diversified portfolio of “local hero” brands that appeal to a wide customer base. With this strategy, Flutter can optimise its market reach and cater to different customer segments through targeted, localised offerings.

Local advertising restrictions, which hinder international competitors from making large media splashes, also work in Flutter’s favour. With Snai and Sisal commanding strong brand loyalty, the company can rely on customer retention and word-of-mouth growth, rather than traditional advertising methods. This creates a high barrier to entry for competitors and gives Flutter the opportunity to solidify its market leadership over the coming years.

Execution risks and regulatory oversight

However, no acquisition is without its risks. The deal is subject to merger control clearance and other regulatory approvals, expected by Q2 2025. Additionally, while Flutter’s history of successful acquisitions is encouraging, integrating Snai into its broader portfolio will require careful management. Achieving the targeted synergies and aligning operational cultures between Snai and Flutter is critical. There is also the broader challenge of navigating Italy’s complex regulatory environment, particularly as the government continues to scrutinise gambling practices and tighten regulations.

Further economic factors, such as rising interest rates, inflation, and consumer sentiment toward gambling, could also affect the pace of integration and future growth. That said, Flutter’s robust financial position and experience navigating heavily regulated markets should help mitigate some of these risks.

Game-changing deal for the industry

Flutter’s acquisition of Snai is more than just a deal to boost market share—it’s a calculated move to solidify the company’s position in Europe’s largest gambling market and pave the way for long-term growth. By combining Snai’s omnichannel reach with Flutter’s technological prowess and experience in executing mergers, the company is well-positioned to capture Italy’s growing online market.

As the transaction unfolds, Flutter’s ability to execute its integration strategy and achieve synergies will be critical. If successful, this acquisition could not only generate significant shareholder value, but also serve as a blueprint for future international expansion, particularly in markets with low online penetration. Flutter has proven it can thrive in competitive environments, and with Snai, it now holds the gold medal in Italy’s gambling industry.

Stay ahead in iGaming! Subscribe to SiGMA’s Top 10 News and Weekly Newsletter for the latest updates and exclusive offers