Better Collective steers through challenges to achieve strong growth in Q2 2024

Better Collective has once again demonstrated its resilience and strategic acumen in the face of change. The Q2 2024 interim report reveals a company adeptly navigating the complexities of its industry while seizing opportunities for growth and innovation. Despite some turbulence, particularly related to recent acquisitions and market shifts, Better Collective’s performance underscores its robust operational framework and forward-looking strategy.

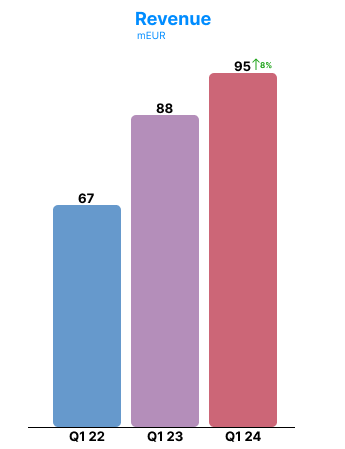

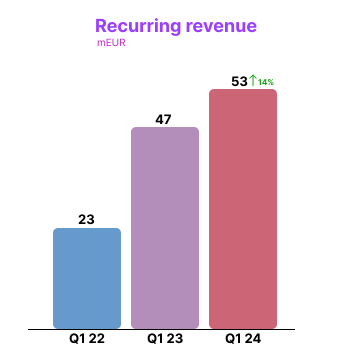

The headline figure from this quarter is the impressive 27 percent revenue growth, reaching 99 million EUR. This is particularly notable given that the same quarter last year saw a staggering 37 percent growth. With 5 percent of this quarter’s growth being organic, it’s evident that the company’s core business remains strong even as it integrates new acquisitions and adjusts to shifting market conditions. The recurring revenue, now standing at 62 million EUR, also saw a significant 26 percent increase, highlighting the company’s success in cultivating stable, ongoing income streams. Recurring revenue now accounts for 62 percent of total revenue, reflecting a deliberate pivot toward more predictable and sustainable business models.

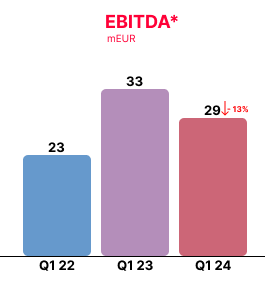

However, not all aspects of Better Collective’s performance were as stellar. EBITDA was flat at 29 million EUR, resulting in a 29 percent margin—a notable decrease from last year’s exceptional 37 percent margin.

This stagnation can be attributed to the recent acquisitions of Playmaker Capital and Playmaker HQ, which have yet to deliver substantial near-term contributions. The integration of these companies has increased costs, particularly in North America, where the backend-loaded seasonality of Playmaker Capital has limited its immediate impact on the bottom line. This, coupled with additional overheads from Canada and underperformance from Playmaker HQ, has diluted the company’s profitability in the short term.

Yet, despite these challenges, Better Collective’s strategic vision remains unshaken. The acquisition of AceOdds during Q2 has already begun to bear fruit, contributing to the company’s upgraded financial targets for 2024. The seamless integration of AceOdds, along with its outperformance in the market, has bolstered Better Collective’s confidence in its growth trajectory. This acquisition has also prompted a share buyback programme, further solidifying the company’s financial foundation and its commitment to delivering value to shareholders.

Another significant development this quarter was the successful mitigation of risks associated with changes in media partnerships, particularly following Google’s policy shifts regarding third-party content. Better Collective managed to fully offset any potential negative impacts, maintaining a net-zero effect on the group’s overall performance.

Resilience and sustainable growth in Q2 2024

This outcome not only underscores the effectiveness of the company’s diversified business strategy but also highlights its ability to adapt swiftly to regulatory and market changes.

The technical advancement of AdVantage, Better Collective’s adtech platform, also marks a key milestone this quarter. With the first proof of concept secured and operational success demonstrated on a small brand, the platform is poised for a broader rollout across the company’s network. While the financial impact for 2024 is expected to be minimal, the long-term potential of AdVantage to drive incremental revenue growth is promising, particularly as it leverages the extended timeline for third-party cookie deprecation.

Looking forward, the underperformance of Playmaker HQ remains a concern, though Better Collective has taken proactive steps to renegotiate the acquisition terms, reducing the final price by 31 million USD. This strategic adjustment, combined with a reshuffling of the commercial team, is expected to improve the brand’s performance in the latter half of the year, albeit with a delayed timeline.

While the challenges of integrating new acquisitions and navigating regulatory changes have impacted short-term profitability, the company’s long-term growth prospects remain robust. With a strong financial position, successful mitigation of external risks, and ongoing innovation, Better Collective is well-positioned to continue its trajectory of sustainable growth.

SiGMA East Europe Summit powered by Soft2Bet, happening in Budapest from 2 – 4 September.